What is a Contractor License Bond and Why You Need One

A contractor license bond is a type of surety bond required by most states and municipalities to ensure contractors operate ethically and comply with licensing laws. This three-party agreement protects the public and provides financial recourse if a contractor fails to meet their legal obligations.

Key Facts About Contractor License Bonds:

- Purpose: Financial guarantee that contractors will follow state regulations and pay workers/suppliers

- Cost: Typically 1-5% of the bond amount (as low as $100 for a $10,000 bond with good credit)

- Duration: One-year terms that must be renewed annually

- Who Needs It: Licensed contractors in most states for trades like electrical, plumbing, HVAC, and general contracting

- Protection: Covers the public, not the contractor—claims must be repaid by the contractor

Bond amounts can range from $5,000 to over $100,000 depending on your state and trade. For example, Oregon requires $20,000 for residential contractors but $75,000 for commercial Level 1 contractors. The federal government also requires bonds for any construction project over $150,000.

Understanding these requirements is crucial because operating without a required bond can result in license suspension, fines, and legal penalties. More importantly, it builds trust with clients who know they have financial protection if something goes wrong.

I’m Haiko de Poel, and I’ve helped scale multiple companies across insurance, fintech, and legal services, giving me deep insight into how contractor license bonds work within regulatory frameworks. My experience with full-stack brand development includes navigating complex licensing requirements that contractors face daily.

What is a Contractor License Bond and Why is it Required?

Think of a contractor license bond as your professional promise backed by financial muscle. It’s a three-party agreement that tells the world you’re serious about following the rules and taking care of your customers. Unlike your truck insurance that protects you, this bond protects everyone else from you – and that’s exactly what makes it so valuable for your business.

When you get bonded, you’re essentially saying, “I’m so confident in my work and integrity that I’m willing to put money on the line.” This creates trust with customers who know they have real recourse if something goes wrong. It’s not just a piece of paper – it’s your ticket to being seen as a legitimate, trustworthy professional.

The bond works as a safety net for everyone you work with. If you abandon a project, don’t pay your suppliers, or cut corners on building codes, the affected parties can file a claim against your bond for financial compensation. This system keeps the construction industry honest and gives consumers confidence to hire licensed contractors.

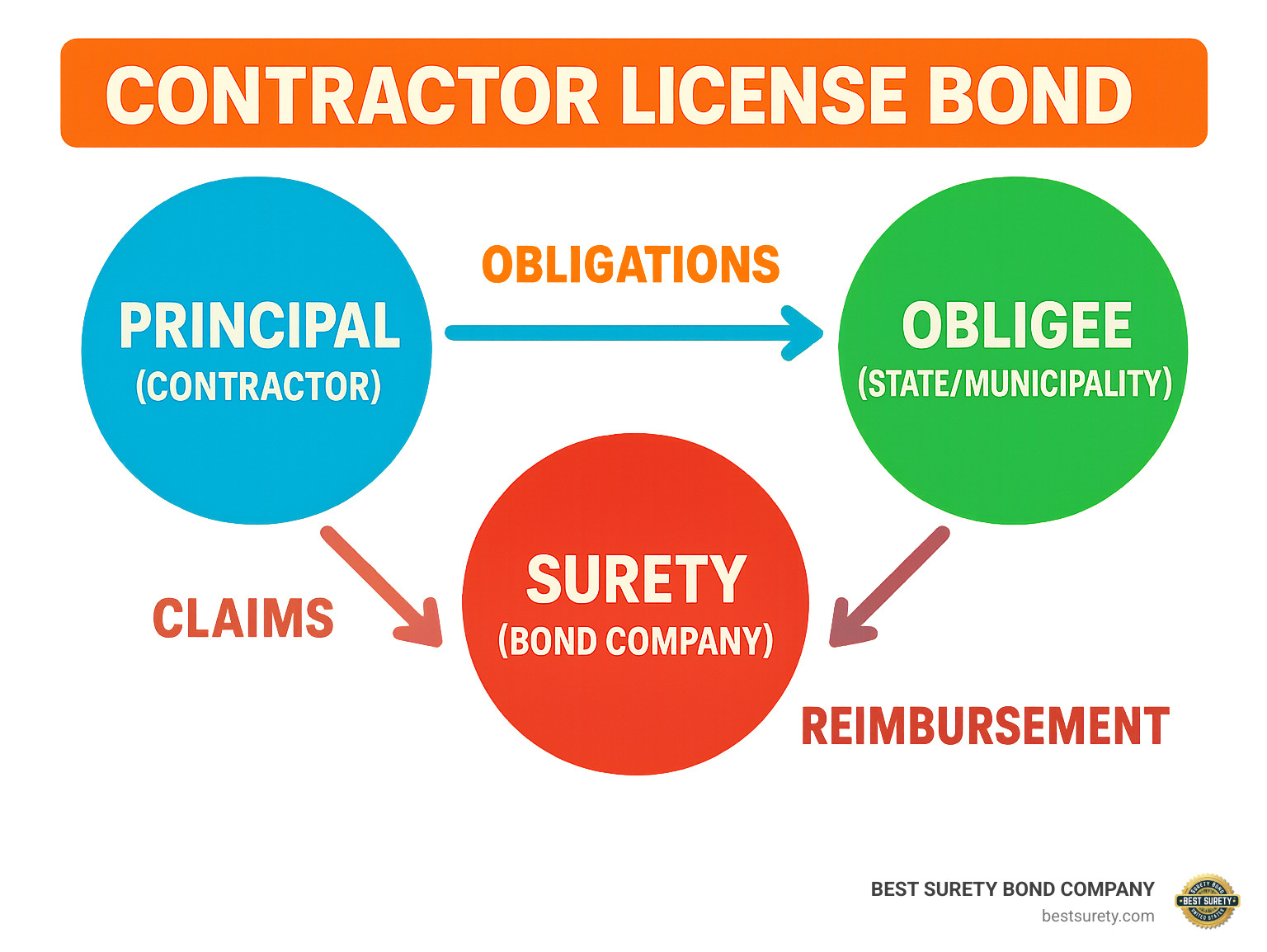

The Three Parties of a Surety Bond

Every contractor license bond brings together three players, each with skin in the game:

You’re the Principal – the contractor who needs the bond. You agree to follow all licensing laws, pay your bills, and complete work according to regulations. If you mess up and a claim gets paid, you owe the surety company every penny back. It’s like having a co-signer on a loan – they might pay initially, but you’re ultimately responsible.

The Obligee is your licensing authority – usually the state board, city, or county that requires the bond. They set the bond amount and can file claims if you violate licensing requirements. Think of them as the referee who made the rules and can call fouls.

The Surety company is your financial backer – that’s companies like BEST SURETY BOND COMPANY. We investigate your creditworthiness and business history, then vouch for your ability to fulfill your obligations. If a valid claim comes in, we investigate and may pay it, but you reimburse us through the indemnity agreement you signed.

This three-way relationship creates accountability while allowing you to get licensed without putting up the full bond amount in cash.

Who Does the Bond Protect?

Your contractor license bond casts a wide protective net over everyone in your professional orbit:

Customers and property owners get peace of mind knowing they can recover losses if you fail to complete work, use substandard materials, or cause damage through code violations. This protection is especially crucial in construction where project costs can reach tens of thousands of dollars.

Subcontractors and material suppliers have recourse when you don’t pay for labor or materials. Instead of chasing you through small claims court, they can file against your bond for faster resolution.

Your employees can seek compensation through the bond if you fail to pay wages or benefits as required by law. This protects workers who might otherwise struggle to recover unpaid compensation.

The general public benefits from protection against fraudulent activities, misrepresentation, or work that doesn’t meet safety standards. Your bond helps ensure public welfare in construction projects.

State licensing agencies can file claims when contractors violate licensing laws, fail to obtain proper permits, or operate outside their licensed scope. This gives regulators teeth to enforce compliance.

Why a Bond is a Prerequisite for Licensing

States and municipalities require contractor license bonds because they’ve learned that voluntary compliance isn’t enough in construction. Here’s why bonding became essential:

Consumer protection tops the list of reasons. The bond provides immediate financial recourse for consumers who might otherwise face years of legal battles to recover losses from problem contractors. In construction, where costs can be substantial and mistakes expensive, this protection is crucial.

Professional standards get enforced through the bonding requirement. Only financially responsible contractors who can qualify for bonds can obtain licenses. This requirement naturally weeds out operators who lack the resources or integrity to complete projects properly.

Public confidence increases when consumers know contractors are bonded. People are more likely to hire licensed, bonded professionals rather than unlicensed operators, which protects both the public and legitimate contractors from unfair competition.

Regulatory compliance improves because contractors know they’ll be financially responsible for violations. When you understand that breaking rules could trigger bond claims you’ll have to repay, you’re much more likely to follow regulations carefully.

Quick dispute resolution becomes possible through the streamlined bond claim process. Rather than forcing consumers into lengthy and expensive lawsuits, the bond provides a faster path to recovering damages and resolving problems.

The bottom line? Your contractor license bond isn’t just a regulatory hurdle – it’s your professional credential that opens doors and builds trust with every customer you meet.

How a Contractor License Bond Works: From Cost to Claims

Getting a contractor license bond is usually far more affordable than contractors expect. Below is a streamlined look at costs, credit considerations, coverage—and what happens if a claim is filed.

What Does a Contractor License Bond Cost?

You never pay the full bond amount. Instead, you pay an annual premium—typically 1%–5% of the required bond limit.

| Credit Tier (Approx.) | Typical Premium |

|---|---|

| Excellent (750+) | 1% |

| Good (650–749) | 1.5%–3% |

| Fair (550–649) | 2%–5% |

| Poor (<550) | 10%+ (specialty programs) |

Other factors—years in business, financial statements, and previous bond claims—can nudge your rate up or down, but credit remains the biggest driver.

Can You Get Bonded with Bad Credit?

Yes. Specialty high-risk programs, premium financing, or adding collateral make bonding possible even with low scores. The rate will start higher, but consistent on-time renewals often qualify you for lower premiums within a year or two.

What the Bond Covers (and What It Doesn’t)

| Covered by the Bond | NOT Covered |

|---|---|

| Failure to pay suppliers or subcontractors | Property damage & bodily injury (handled by General Liability) |

| Unpaid employee wages | Workers’ compensation claims |

| Building-code or permit violations | Poor workmanship that does not violate code |

| Fraudulent acts / misrepresentation | Contract disputes over timeline or aesthetics |

| Operating outside licensed scope | Equipment loss, theft, weather delays |

The bond protects the public and regulators—not you. If a claim is paid, you reimburse the surety under your indemnity agreement.

The Claim Process in Four Short Steps

- Claim filed with documentation.

- Surety investigates and notifies you.

- Resolution attempt—most disputes settle here when contractors provide proof or make things right.

- Payment & Indemnity—if the claim is valid and unresolved, the surety pays up to the bond limit and then seeks reimbursement from you.

Avoiding claims protects both your wallet and your ability to qualify for future bonds at the best rates.

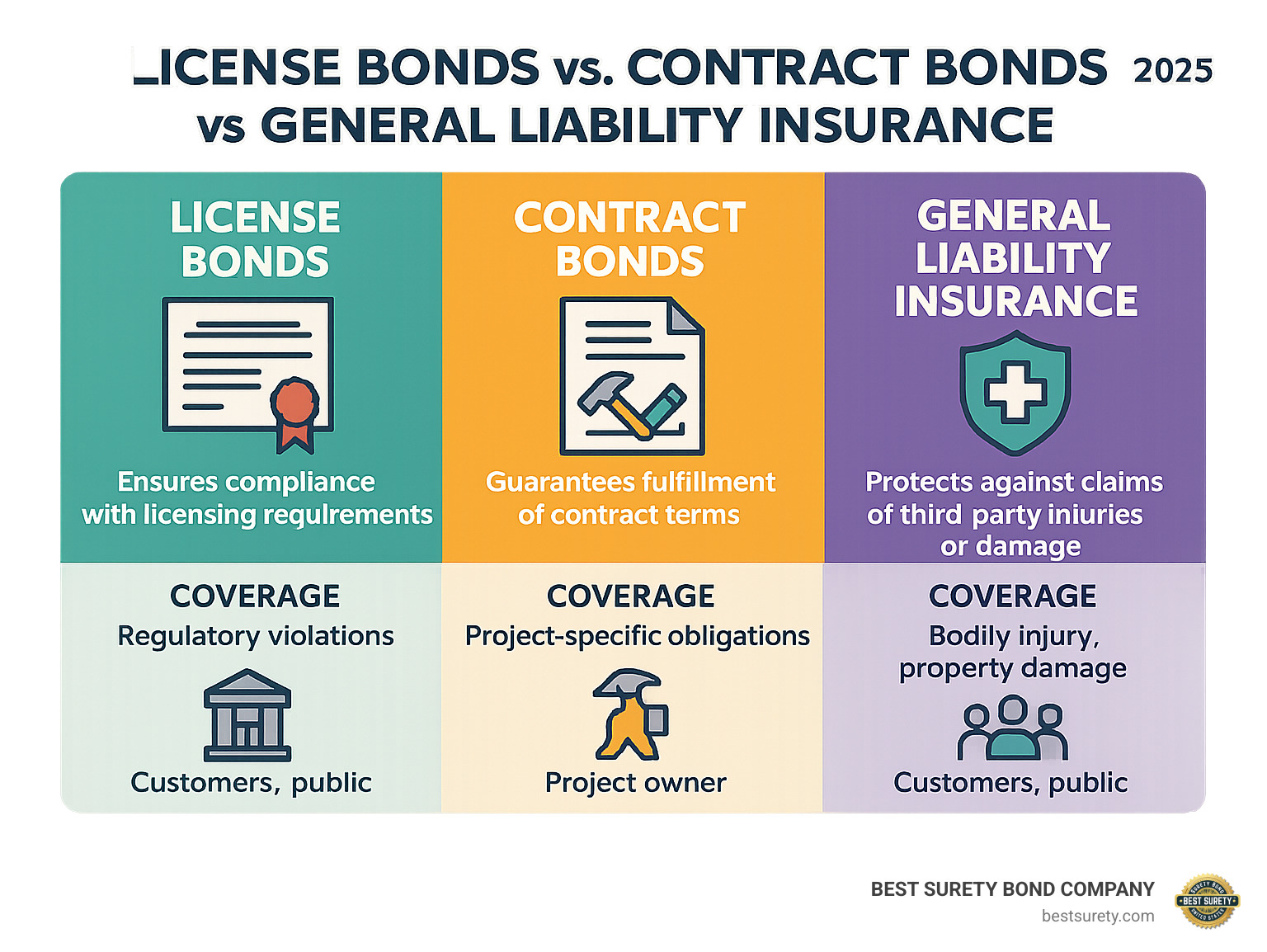

Contractor License Bonds vs. Other Construction Bonds and Insurance

Navigating contractor bonds and insurance can feel overwhelming, especially when you’re trying to understand what you actually need for your business. The good news is that each type of coverage serves a specific purpose, and understanding these differences will help you make smarter decisions about protecting your contracting business.

Think of it this way: contractor license bonds are like your professional ID card that proves you’re trustworthy enough to hold a license, while contract bonds are project-specific guarantees, and insurance protects you from the unexpected things that can go wrong on any job site.

Contractor License Bond vs. Contract Bonds

Here’s where many contractors get confused – and it’s totally understandable. Both are bonds, but they serve completely different purposes in your business.

Your contractor license bond is essentially your ticket to stay in business. It’s required by your state or municipality just to hold your contractor license, and it covers all the work you do throughout the year. Think of it as your ongoing promise to follow the rules – paying suppliers, following building codes, and operating within your licensed scope.

Contract bonds, on the other hand, are project-specific guarantees that protect individual project owners. When you bid on a large commercial project or government contract, you might need a bid bond to show you’re serious about the project, a performance bond to guarantee you’ll complete the work, and a payment bond to ensure you’ll pay your subcontractors and suppliers.

The key difference? Your license bond follows you everywhere and protects the public, while contract bonds are tied to specific projects and protect the project owner. License bonds are relatively affordable – often just a few hundred dollars annually – while contract bonds can cost thousands depending on the project size.

Most contractors need their license bond first, since you can’t even get licensed without it. Contract bonds become important as you grow and pursue larger projects, especially government work where they’re typically required for any project over $150,000.

How a Contractor License Bond Differs from Insurance

This is probably the most important distinction to understand, because mixing up bonds and insurance can leave you with serious coverage gaps.

A contractor license bond is fundamentally different from insurance because it’s a three-party agreement. You’re the principal, the licensing authority is the obligee, and we’re the surety. The bond guarantees you’ll follow licensing laws, but if someone files a claim and we pay it, you have to pay us back. The bond protects others from your actions, not the other way around.

Insurance, however, is a two-party agreement between you and an insurance company. When you pay your premium, you’re transferring risk to the insurer. If someone gets hurt on your job site and files a claim against your general liability insurance, the insurance company handles it and you don’t have to repay them (assuming it’s a covered claim).

Workers’ compensation insurance is a perfect example of why you need both. If an employee gets injured, workers’ comp covers their medical bills and lost wages. But if you fail to carry workers’ comp as required by law, that’s a licensing violation that could trigger a claim against your contractor license bond.

General liability insurance protects you when accidents happen – like if you accidentally damage a customer’s property or someone gets hurt because of your work. Your license bond doesn’t cover these situations at all.

The bottom line? Your contractor license bond ensures you follow the rules, while insurance protects you when things go wrong despite following the rules. You need both to run a successful contracting business, and neither one can replace the other.

At BEST SURETY BOND COMPANY, we help contractors across Texas and nationwide understand exactly what bonds they need and get approved quickly. Whether you need a basic license bond or you’re ready to pursue larger projects requiring contract bonds, we’ll guide you through the process and get you bonded fast.

How to Get Your Contractor License Bond: A State-by-State Overview

Bond requirements change from state to state—and sometimes city to city—but securing the bond itself is fast once you know the exact amount and obligee. Here’s the condensed playbook that works nationwide.

The 3-Step Fast-Track to Getting Bonded

- Determine Requirements – Confirm state, county, or municipal bond amounts and the correct obligee name.

- Apply for a Quote – Complete our short online form. Standard applications receive same-day approval.

- Pay & File – Pay securely online and receive original bond documents instantly to file with your licensing agency.

Total turnaround for most contractors: a few hours from application to filed bond.

How Requirements Differ by State

Bond limits range from $5,000 in some jurisdictions to $75,000 or more for high-risk commercial work. A few quick highlights:

- California – Flat $25,000 license bond for all classifications.

- Oregon – Dual system: $20,000 residential vs. up to $75,000 commercial.

- Nevada – Separate specialty bonds (e.g., pool & spa) in addition to the primary license bond.

- Alaska – $5,000–$25,000 depending on contractor type.

Always verify the current bond form and wet-signature rule—some states now accept e-filing, but most still require originals.

What About Texas?

Texas has no state-level license bond, but dozens of cities do. Examples:

- Houston – Trade-specific municipal bonds.

- Dallas – Bonds for specialty trades and some public-right-of-way work.

- Austin and San Antonio – Local bonds for certain contractor classes.

Because local rules vary, step one is calling the city building department to confirm the bond amount. Once you have that figure, we routinely deliver same-day approval for Texas municipal bonds—keeping you compliant and on the job without delay.

Frequently Asked Questions about Contractor License Bonds

How long does it take to get a contractor license bond?

The great news is that getting your contractor license bond doesn’t have to slow down your business plans. With our streamlined online application process, most contractors receive their bond documents the same day they apply – sometimes within just a few hours.

Here’s what you can expect: Application reviews typically take 1-2 hours for standard applications, while underwriting happens the same day for contractors with good credit. Once approved, we deliver your bond documents immediately through electronic delivery, so you can file with your licensing authority right away.

Even if you have credit challenges or a more complex business situation, we usually complete underwriting within 1-2 business days. We understand that time is money in the construction business, so we’ve designed our process to get you licensed and working as quickly as possible.

Do contractor license bonds need to be renewed?

Yes, most contractor license bonds have one-year terms and must be renewed annually to keep your contractor license active and in good standing. Think of it like renewing your driver’s license – it’s a regular part of maintaining your professional credentials.

We make the renewal process painless by sending you renewal reminders 60-90 days before your bond expires. Many of our contractors with good payment history qualify for automatic renewal, which means no paperwork hassles or last-minute scrambling.

Your annual renewal is also a great opportunity for a rate review – if your credit has improved or your business has grown stronger, you might qualify for better premium rates. The key is maintaining continuous coverage because even a brief lapse can trigger immediate license suspension.

Important reminder: Don’t let your bond expire! A lapsed bond can result in fines, license suspension, and the inability to work legally until you’re bonded again.

What happens if I don’t have a contractor license bond?

Operating without a required contractor license bond is like driving without a license – the consequences can be swift and severe. We’ve seen too many contractors learn this lesson the hard way, so let’s talk about what’s really at stake.

Legal penalties hit first and hit hard. Your license can be suspended or revoked immediately, which means no permits, no legal work, and potential criminal charges for unlicensed contracting. Licensing authorities don’t mess around with bond requirements.

The business impact ripples through everything you do. Existing contracts that require licensed contractors can be canceled, you can’t bid on new projects, and your professional reputation takes a serious hit. Word travels fast in the construction industry.

Financial consequences might hurt the most. Customers can refuse to pay for work done by unlicensed contractors, and in many states, you have no legal recourse to collect payment. You’re also personally liable for damages without bond protection, and insurance companies may raise your premiums due to increased risk.

Public safety is ultimately why these bonds exist. Without a bond, consumers who hire you have no financial protection, which increases the risk of substandard work and potential harm to public welfare.

The bottom line is simple: The cost of a bond is minimal compared to the risks of operating without one. Getting bonded protects your business, your customers, and your professional reputation. At BEST SURETY BOND COMPANY, we make it fast and affordable to stay compliant and keep your business thriving.

Get Bonded Today and Build with Confidence

Getting your contractor license bond is one of the smartest investments you can make for your contracting business. It’s not just about checking a legal box – it’s about building the trust and credibility that separates professional contractors from the competition.

When customers see that you’re properly bonded, they know you’re serious about your work and financially accountable for your actions. This peace of mind often makes the difference between winning and losing contracts, especially for larger projects where clients want assurance they’re working with established professionals.

The bonding process is much simpler than most contractors expect. With our streamlined online application, you can get approved and receive your bond documents the same day. Fast approvals mean you don’t have to wait weeks to get licensed and start working. For most contractors with decent credit, the entire process takes just a few hours from application to filing.

Cost shouldn’t be a barrier either. Premium rates typically start at just 1% of the bond amount for contractors with excellent credit. Even if your credit isn’t perfect, you can still get bonded – we specialize in finding solutions for contractors with challenging financial situations. When you consider that a $10,000 bond might cost just $100 annually, it’s a small price to pay for the professional credibility and legal protection it provides.

Texas contractors have the advantage of working with a local company that understands the unique requirements across all Texas counties. From Houston’s municipal bonds to Dallas specialty trade requirements, we know exactly what documentation you need and where to file it. Our Texas expertise combined with national reach means we can support your business whether you’re working locally or expanding to new states.

What sets BEST SURETY BOND COMPANY apart is our commitment to combining personal service with digital convenience. You can start your application online and get instant quotes, but you’ll also have access to licensed agents who understand your business and can guide you through any complex situations. We’ve bonded over 10,000 clients and earned BBB accreditation by making the process fast, affordable, and straightforward.

Don’t let bonding requirements become a roadblock to your success. The contractors who get bonded quickly are the ones who can bid on the best projects, build stronger client relationships, and grow their businesses with confidence. Whether you’re getting your first license or expanding to new markets, having the right bond is essential for long-term success.

Get Your Instant Contractor Bond Quote Now!

Ready to move forward? Our licensed agents are standing by to help you steer the requirements and get approved quickly. With same-day processing available for most applications and competitive rates starting at just 1%, there’s no reason to delay. Get bonded today and start building your business with the confidence that comes from proper licensing and professional credibility.